The laws relating to the Partnership form of business is contained in the Indian Partnership Act, 1932. In this article we shall discuss and understand in brief the nature and overview of partnership form of business..

Table of Contents

Introduction

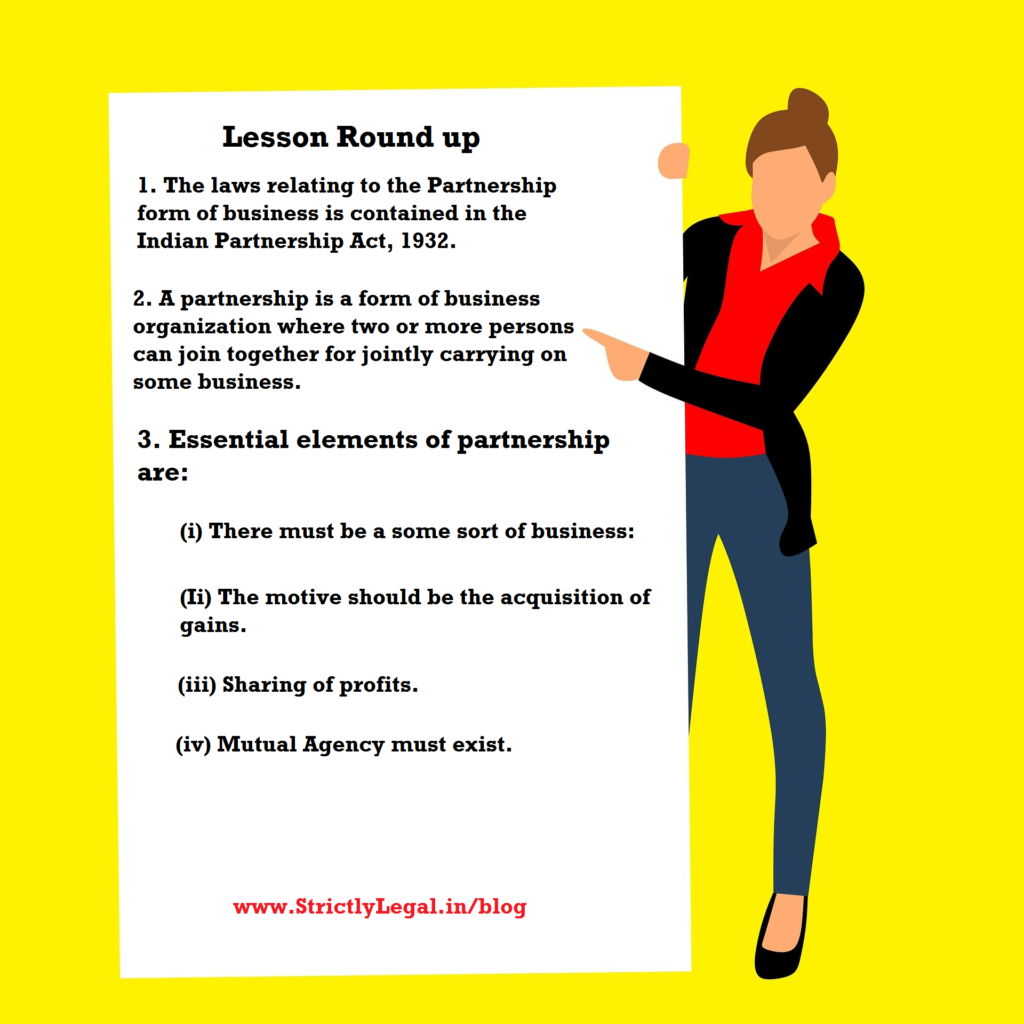

The laws relating to the Partnership form of business is contained in the Indian Partnership Act, 1932.

The Indian Partnership Act was enacted in 1932 and it came into force on the 1st day of October 1932. The present Act superseded the earlier law relating to Partnership, which was contained in Chapter XI of The Indian Contract Act, 1872.

It is to be noted that this Act is not exhaustive in nature.

Offer and acceptance, consideration, free consent, the legality of Object, etc. are the contents of the Indian Contract Act and are also applicable to the contract of Partnership.

A partnership is a form of business organization where two or more persons can join together for jointly carrying on some business. In a Partnership, the profit or loss is distributed amongst the partners as agreed upon at the time of entering the partnership agreement; if not the profit and loss is usually equally shared.

The Persons who have entered into a partnership with one another are called individually as ‘partners’, and collectively ‘a firm’, and the name under which their business is carried on is called the ‘firm name’.

Definition of Partnership

Section 4 of the Indian Partnership Act, 1932 defines Partnership as:

‘Partnership’ is the relationship between persons who have agreed to share the profit of a business carried on by all or any of them acting for all.

The Calcutta High Court explained the term ‘Partnership’ in the Registrar of Firms, Societies and Non-Trading Corporation, West Bengal & another v. Tarun Manna & others, and according to the court, the partnership is the relation between persons created by contract whereby the parties to such contract have agreed to share the profits of the business with a further condition that the proposed business must be carried out by all or any of them acting for all.

Therefore, the first condition of the existence of the partnership is that there must be an agreement by the partners to share the profit of a business. The other condition is that such business must be agreed to be carried on by all of them, or any of them acting for all.

In other words, there must be the existence of an agency among the partners of the proposed business as specifically recognized in Section 18 of the Indian Partnership Act, 1932.

Essentials of Partnership

According to Section 4, the following essentials are necessary to constitute a ‘partnership’ :

Association of two or more persons. A single person cannot form a partnership.

- There should be an agreement between the persons who want to be partners. Not necessarily written though.

- The purpose of creating a partnership should be carrying on of the business.

- The motive for the creation of partnerships should be earning and sharing profits.

- The business of the firm should be carried on by all of them or any of them acting for all, i.e., in a mutual agency.

- When all the above elements/legal requirements are present in a certain relationship that is known as partnership.

An Agreement

All the persons concerned must have entered into an Agreement. The agreement here means a contract. The nature of the partnership is voluntary and contractual.

It is the element of the agreement that distinguishes it from other forms of associations like members of a joint family, joint owners, etc. The existence of a contract is sine qua non of the relationship of partnership.

Neither can it be inherited. A partnership does not arise from status, operation of law, or inheritance. Thus at the death of the father, who was a partner in a firm, the son can claim a share in the partnership property but cannot become a partner unless he enters into a contract for the same with other persons concerned.

Hence, a partnership does not arise from status, operation of law, or inheritance.

An agreement from which relationship of partnership arise may be express or implied from the act done by the partners and from a consistent course of conduct being followed showing mutual understanding between them.

It may be oral or in writing. The duties and powers of various partners should be clearly defined and should be in writing. Sometimes such an agreement is even implied by the continued actions and mutual understanding of the partners.

Carrying on Actual Business

Another essential element of a partnership is that it is formed to carry on some business that is legal. An association or society formed primarily to carry on some charitable, religious, or social works cannot be regarded as a partnership.

Even co-ownerships does not amount to a partnership.

In this context we consider two terms:

There must be a business:

The term business according to Section 2(b) of the Indian Partnership Act,1932 includes every trade, occupation, and profession.

Thus, business is used in its widest sense as it does not refer merely to trade or industry but also includes occupations and professions such as chartered accountancy, legal practice, placement services, etc.

However, the business doesn’t need to consist of a protracted (i.e., long-lasting) and permanent undertaking. An agreement to carry on a business at a future time may not be considered as a partnership until the actual time has arrived and the business is started.

The business must be in existence and being carried on. The term ‘carried on’ suggests continuity or repetition of acts. Merely a single isolated transaction of purchase and sale by a number of persons does not mean carrying on of the business.

if a number of articles are purchased at one time and the sales are to go on, profits are to be realized and are to be divided amongst a number of persons, there is a carrying on of a business.

The motive should be acquisition of gains:

It leads to the formation of the partnership and the intention to share the profit should be significantly original and influential. The ultimate aim of the business should be to make gains, which are then distributed among the partners.

So a firm carrying on charitable work will not be a partnership. If there is no intention to earn profits, there is no partnership.

Sharing of profits

Sharing the profits of business amongst all the partners is the core of the partnership. Profit here means net profit, i.e., excess of returns over outlays, the excess of what is obtained over the cost of obtaining it.

This essential element provides that the agreement to carry on business must be with the object of sharing profits amongst all the partners. Impliedly the partnership must aim to make profits because then only profits may be divided amongst the partners.

There can be no partnership where only one of the partners is entitled to the whole of the profits of the business. Partners should choose to share the profits in the manner pre-determined or equally.

But an agreement to share losses is not an essential element. It is open to one or more partners to agree to share all the losses. However, in the event of losses, unless agreed otherwise, these must be borne in the profit-sharing ratio. Thus, one can become a partner on the understanding that he will not share the losses.

Though sharing of profits is one of the essentials of partnership, it still cannot be said be a conclusive proof of the existence of partnership.

Mutual Agency

The cardinal principle of the partnership law is that the business must be carried on by all partners or by any one of the partners as acting for all. There should be a binding contract of mutual agency between the partners.

It is the mutual agency which gives the concerned persons the status of the owner of the business, and the notion of mutual trust that the partners are expected to keep with each other.

It is an extension of the principle of agency. The true test of partnership is mutual agency and not sharing of profits. An act of one partner is the act of all the other partners in the course of the firm.

Each of the partners is the principle as well as the agent of all the other. The public has a right to assume that every partner has authority from his co-partners to bind the whole firm in contracts made according to the ordinary usage of trade.

The importance of the element of mutual agency lies in the fact that it enables every partner to carry on the business on behalf of others. Partners may agree among themselves that someone of them shall not enter into any contracts on behalf of the firm, but by virtue of the principle of mutual agency, such partner can bind the firm vis-a-vis third parties without notice in contracts made according to the ordinary usage of trade.

To test whether a person is a partner or not, it should be seen, among other things, whether or not the element of agency exists, whether the business is conducted on his behalf.

To determine whether a person is a partner or not is to see inter-alia, whether the relationship of principal and agent exists between the parties. in fact, the existence of the element of agency is the foundation of partnership which is regarded as an extension of the general law of agency.

Contributions such as these help us build and sustain a community of curious minds. We welcome Contributors to Sign up on our website through this link and send us their articles or blog posts.

This article was Co-contributed by Aishwaria Agarwal from Indian Institute of Legal Studies, Siliguri

Striving to create a community of like minds,

team SL,

Users not registered with Strictlylegal can Email us their content and the same are posted through this account. In case of abuse, kindly let us know at [email protected]